Breaking News

You better sit down for this one: here's how Biden regime got illegals on commercial flights…

You better sit down for this one: here's how Biden regime got illegals on commercial flights…

If Trump Does Not Go To War With Iran, We Will Need To Thank One Man

If Trump Does Not Go To War With Iran, We Will Need To Thank One Man

Rising Capital Controls, Tighter Borders, and What You Can Do About It

Rising Capital Controls, Tighter Borders, and What You Can Do About It

The substitution of a tariff for the income tax would re-create free Americans

The substitution of a tariff for the income tax would re-create free Americans

Top Tech News

US particle accelerators turn nuclear waste into electricity, cut radioactive life by 99.7%

US particle accelerators turn nuclear waste into electricity, cut radioactive life by 99.7%

Blast Them: A Rutgers Scientist Uses Lasers to Kill Weeds

Blast Them: A Rutgers Scientist Uses Lasers to Kill Weeds

H100 GPUs that cost $40,000 new are now selling for around $6,000 on eBay, an 85% drop.

H100 GPUs that cost $40,000 new are now selling for around $6,000 on eBay, an 85% drop.

We finally know exactly why spider silk is stronger than steel.

We finally know exactly why spider silk is stronger than steel.

She ran out of options at 12. Then her own cells came back to save her.

She ran out of options at 12. Then her own cells came back to save her.

A cardiovascular revolution is silently unfolding in cardiac intervention labs.

A cardiovascular revolution is silently unfolding in cardiac intervention labs.

DARPA chooses two to develop insect-size robots for complex jobs like disaster relief...

DARPA chooses two to develop insect-size robots for complex jobs like disaster relief...

Multimaterial 3D printer builds fully functional electric motor from scratch in hours

Multimaterial 3D printer builds fully functional electric motor from scratch in hours

WindRunner: The largest cargo aircraft ever to be built, capable of carrying six Chinooks

WindRunner: The largest cargo aircraft ever to be built, capable of carrying six Chinooks

RNA Crop Spray: Should We Be Worried?

RNA Crop Spray: Should We Be Worried?

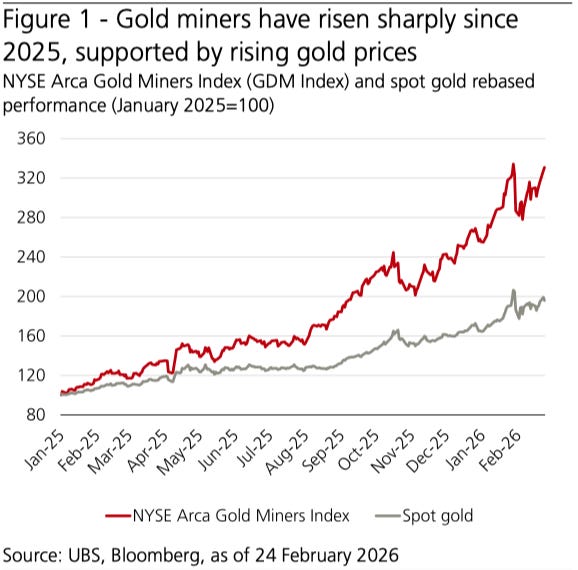

UBS Has a 3 Pillared Thesis on Gold Miners

The thesis rests on three reinforcing pillars: sustained gold demand, materially improved corporate fundamentals, and contained production costs.

-UBS

UBS (less specifically but equally bullish compared to the JPM outlook yesterday) sees gold mining equities are rebounding alongside strengthening bullion fundamentals, with gold projected toward $5,900/oz on sustained central bank demand, ETF inflows, and easing real rates. UBS has a 3-pronged thesis on why it should continue for 2026. Improved margins, falling leverage, and tighter capital discipline support valuations. Includes a list of miners meeting their criteria for this continued run.

Gold Mining Equities: Tactical Re-Engagement Within a Structural Bull Cycle

Gold mining equities have begun the year with strong performance, rising approximately 30% year to date after recovering from a sharp late-January correction. The sector's rebound has coincided with renewed strength in bullion prices and re-accelerating investor demand for precious metals exposure. The authors frame this move as more than a reflexive bounce. They identify three drivers supporting a tactical opportunity in the mining complex: sustained bullion strength, improved corporate fundamentals, and contained production costs.

The constructive outlook begins with bullion itself.

"We continue to rate gold as Attractive and remain 'long' the metal within our global asset allocation."

The expectation is for gold to trade around USD 5,900 per ounce by year-end. The support structure cited includes continued central bank demand, ongoing ETF inflows, declining real US interest rates, and persistent geopolitical risk. The authors characterize gold as being in the mid-to-late phase of its current bull market, a stage typically marked by new highs interspersed with mid- to high single-digit pullbacks.

Crucially, they argue that the macro conditions historically associated with the end of gold bull markets have not materialized.

"The conditions that have historically marked the end of gold bull markets—persistently elevated real interest rates, a structurally stronger US dollar, an improved geopolitical backdrop, and fully restored central bank credibility—have yet to materialize."

With two additional Federal Reserve rate cuts expected this year, policy is viewed as remaining supportive. Real rate compression continues to serve as a tailwind rather than a headwind.

Demand data reinforces the positioning. World Gold Council figures indicate that total gold demand exceeded 5,000 metric tons for the first time in 2025. Investment flows and central bank accumulation remain core pillars of demand. The authors have revised their 2026 demand forecasts higher, citing expectations for stronger ETF inflows and resilient physical demand across bars, coins, and jewelry.